sys.path.append("/home/quant/Documents/Use-Cases")

from engine import Engine

from strategies.rsi2 import RSI2MeanReversion

from strategies.rsi2_final import RSI2MeanReversionFinal

engine = Engine(init_cash=100_000, fees=0.0, fixed_fees=0.0, slippage=0.0000

close = engine.load_data_yf("QQQ", period="max", interval="1d", field="Close

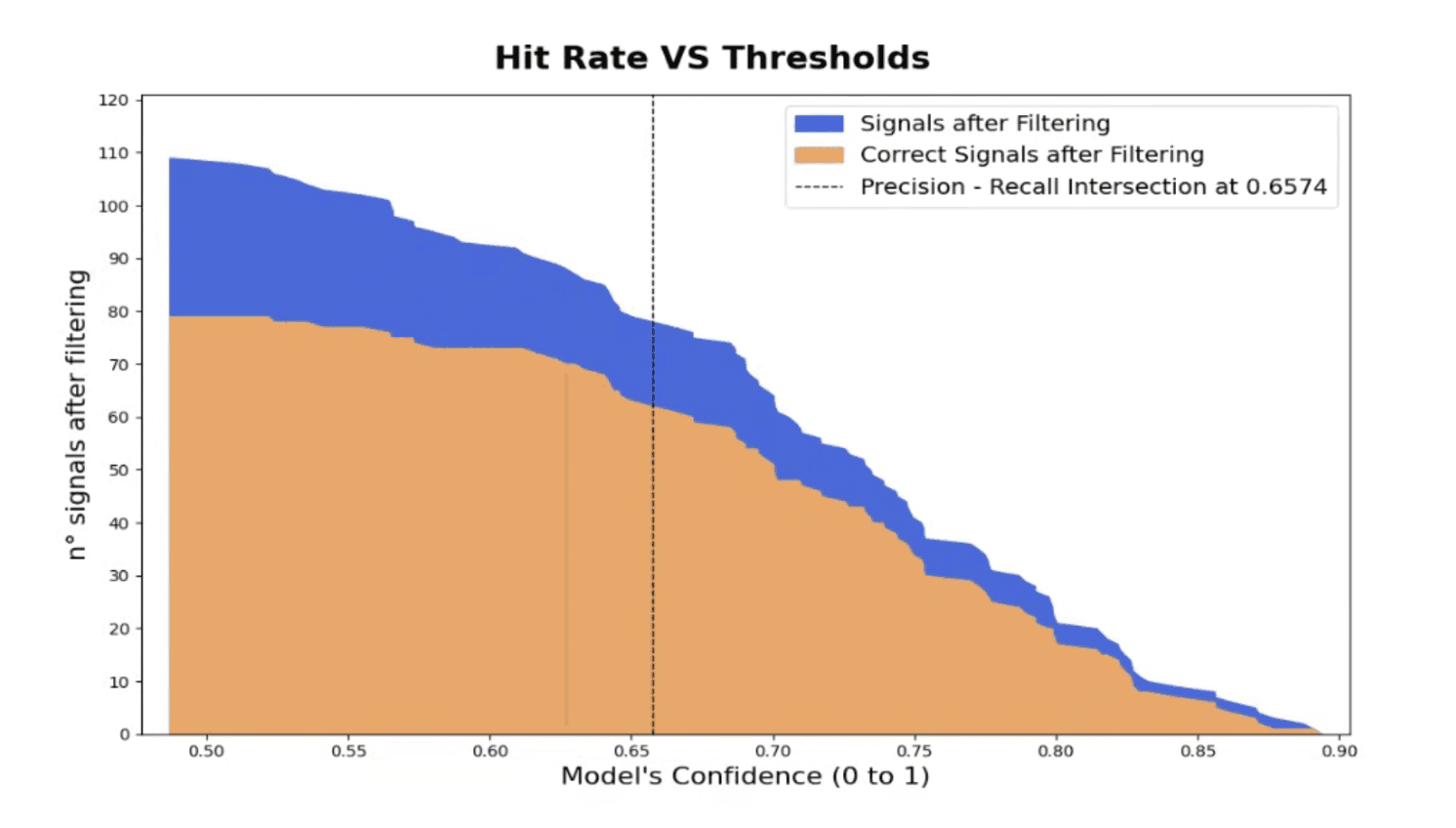

filter_csv = "/mnt/Share8TB/use_cases/Strategy2/Report_2025_10_21__15_39_40/

csv_start, csv_end = engine.apply_prediction_window_from_csv(

csv_path=filter_csv,

prediction_dt_col="PredictionDT",

warmup_days=300,

per_share_fee=0.0035,

)

base = RSI2MeanReversion(

rsi_buy_long=10,

rsi_sell_long=70,

rsi_sell_short=90,

rsi_cover_short=30,

sma_window=200,

)

signals_path_base = "/home/quant/Documents/Use-Cases/signals_csvs/baseline/s

plot_path_base = "/home/quant/Documents/Use-Cases/equity_curves/baseline/equ

os.makedirs(os.path.dirname(signals_path_base), exist_ok=True)

os.makedirs(os.path.dirname(plot_path_base), exist_ok=True)

pf_base = engine.run_backtest(base, export_csv_path=signals_path_base, start

strat_thr = RSI2MeanReversionFinal(

rsi_buy_long=10,

rsi_sell_long=70,

rsi_sell_short=90,

rsi_cover_short=30,

sma_window=200,

prediction_csv_path=filter_csv,

prediction_dt_col="PredictionDT",

score_col="QuantedModelPredictions",

score_threshold=0.6,

force_exit_at_end=True,

)

signals_path_thr = "/home/quant/Documents/Use-Cases/signals_csvs/filtered_co

os.makedirs(os.path.dirname(signals_path_thr), exist_ok=True)

pf_thr = engine.run_backtest(strat_thr, export_csv_path=signals_path_thr)

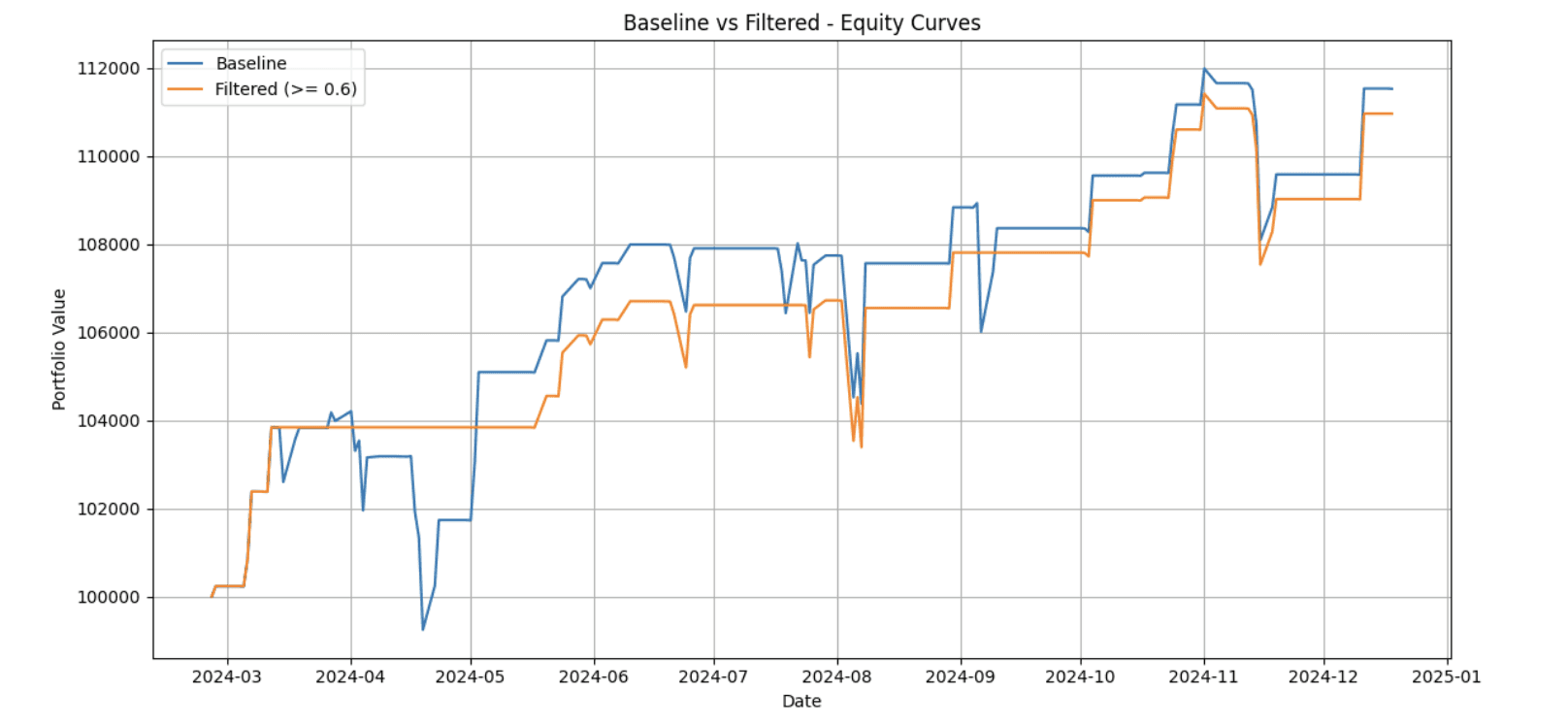

combined_dir = "/home/quant/Documents/Use-Cases/equity_curves/combined"

os.makedirs(combined_dir, exist_ok=True)

combined_path = os.path.join(combined_dir, "equity_curve_strat2_combined.png

engine.plot_equities(

[

("Baseline", pf_base),

(f"Filtered (>= {strat_thr.score_threshold})", pf_thr),

],

path=combined_path,

show=True,

title="Baseline vs Filtered - Equity Curves",

normalize_to=100000.0,

)

print("Side-by-side Comparison")

stats_base = pf_base.stats()

stats_thr = pf_thr.stats()

thr = getattr(strat_thr, "score_threshold", None)

common = [

"Total Return [%]", "Sharpe Ratio", "Calmar Ratio", "Sortino Ratio",

"Max Drawdown [%]", "Max Drawdown Duration", "Win Rate [%]",

"Total Trades", "Profit Factor"

]

comp = pd.DataFrame({

"Baseline strategy": stats_base.reindex(common),

f"Quanted ML filtered (>= {thr})": stats_thr.reindex(common),

}).round(2)

comp["Δ% (Filtered vs Baseline)"] = (

(comp.iloc[:, 1] - comp.iloc[:, 0]) / comp.iloc[:, 0].replace(0, np.nan)

).round(2)

col_base = "Baseline strategy"

col_filt = f"Quanted ML filtered (>= {thr})"

rows_pct = ["Total Return [%]", "Max Drawdown [%]", "Win Rate [%]"]

rows_num = ["Sharpe Ratio", "Calmar Ratio", "Sortino Ratio", "Total Trades",

row_dur = ["Max Drawdown Duration"]

def fmt_timedelta(v):

if pd.isna(v):

return ""

return f"{(v / pd.Timedelta(days=1)):.2f} days" if isinstance(v, pd.Time

styled = (

comp.style

.format("{:+.2f}%", subset=pd.IndexSlice[:, ["Δ% (Filtered vs Baseli

.format("{:.2f}%", subset=pd.IndexSlice[rows_pct, [col_base, col_fil

.format("{:.2f}", subset=pd.IndexSlice[rows_num, [col_base, col_filt

.format(fmt_timedelta, subset=pd.IndexSlice[row_dur, [col_base, col_

)